Down 49% in 2026, Is Whirlpool Stock Undervalued or a Value Trap?

Key Takeaways:

- Margin Reset Underway: Whirlpool announced its largest price increase in a decade — more than 10% — to restore profitability in North America.

- Price Projection: Based on current assumptions, WHR stock could reach $46.34 by December 2028.

- Potential Gains: That target implies a total return of 21.6% from the current price of $38.10.

- Annual Return: Investors could see roughly 8.1% annualized growth over the next 2.5 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Whirlpool (WHR) is going through one of the roughest stretches in its history. The stock has fallen 65% over the past year and trades near multi-decade lows.

- Revenue has declined every year for the past four years.

- Operating margins sit at just 4.7%.

- Q1 2026 made things worse before they get better.

- The U.S. appliance industry fell 7.4% in the quarter, with March alone down 10% — a level of contraction not seen since the global financial crisis.

- Consumer sentiment hit a 50-year low as discretionary demand collapsed.

- Whirlpool delivered an ongoing EBIT margin of just 1.3% and reported an adjusted loss per share of $0.56.

CEO Marc Bitzer was direct: Q1 was a tough quarter driven by external shocks. But the company is not sitting still.

See analysts’ full growth forecasts and estimates for WHR stock (It’s free) >>>

What the Model Says for Whirlpool Stock

We analyzed Whirlpool through the lens of a deeply cyclical business that is taking aggressive steps to reset its cost structure and pricing power.

The core thesis is straightforward. More than 60% of U.S. appliance demand is replacement-driven — people whose washer breaks don’t have a choice about buying a new one. That demand doesn’t disappear; it only gets delayed.

What collapsed in Q1 was discretionary demand: consumers choosing to upgrade rather than replace. That part of the market is highly sensitive to confidence, and confidence is currently at historic lows.

The pricing actions are meaningful. On April 17, Whirlpool implemented a promotional price increase of over 10% versus Q1 pricing. A second wave — an additional 4% list price increase — is set for July 9.

Management says the first two weeks of consumer-visible pricing following the announcement were encouraging. Competitors have also shifted toward more rational pricing behavior, especially after new Section 232 tariff rules now require a flat 25% tariff on all imported appliances regardless of origin.

That change is structurally helpful for Whirlpool, which manufactures roughly 80% of what it sells in the U.S.

- On the cost side, Whirlpool is targeting over $150 million in savings in 2026.

- A new $60 million facility in Perrysburg, Ohio should deliver $30 million in annualized EBIT.

- Modernization of the Amana, Iowa plant is expected to add another $70 million annually.

- These savings carry forward into 2027 and beyond.

The one clear bright spot is the KitchenAid Small Appliances business, which grew revenue roughly 10% year-over-year and expanded EBIT margins by 250 basis points to 21% in Q1. It’s now in its sixth consecutive quarter of year-over-year revenue growth.

Using a forecast of 1.2% annual revenue growth and 4.8% operating margins, with an exit P/E of 9.5x, our model projects WHR reaching $46.34 by December 2028. That’s a 21.6% total return, or 8.1% annualized.

The 9.5x P/E assumption is in line with WHR’s five-year and ten-year historical averages of 9.5x, making it a reasonable middle-ground assumption.

Our Valuation Assumptions

WHR Stock Valuation Model (TIKR)

WHR Stock Valuation Model (TIKR)

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for WHR stock:

1. Revenue Growth: 1.2%

WHR revenues have declined 6.5% over the past year and contracted at a 4.4% annual rate over five years.

The 1.2% assumption reflects a gradual stabilization rather than a sharp rebound.

Management guided full-year 2026 revenue growth of approximately 1.5% on a like-for-like basis, so this assumption is roughly in line with near-term expectations.

2. Operating margins: 4.8%

Trailing EBIT margins are 4.7%.

The model assumes only a modest improvement to 4.8% — conservative given management’s stated path toward 9% in the longer term.

The price increases and $150 million cost program should begin flowing through in the second half of 2026, with more meaningful impact in 2027.

3. Exit P/E Multiple: 9.5x

WHR currently trades at 10.8x forward earnings.

The model assumes slight compression to 9.5x, consistent with the stock’s three- and ten-year historical averages.

Limited multiple expansion is assumed here, keeping the forecast grounded.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

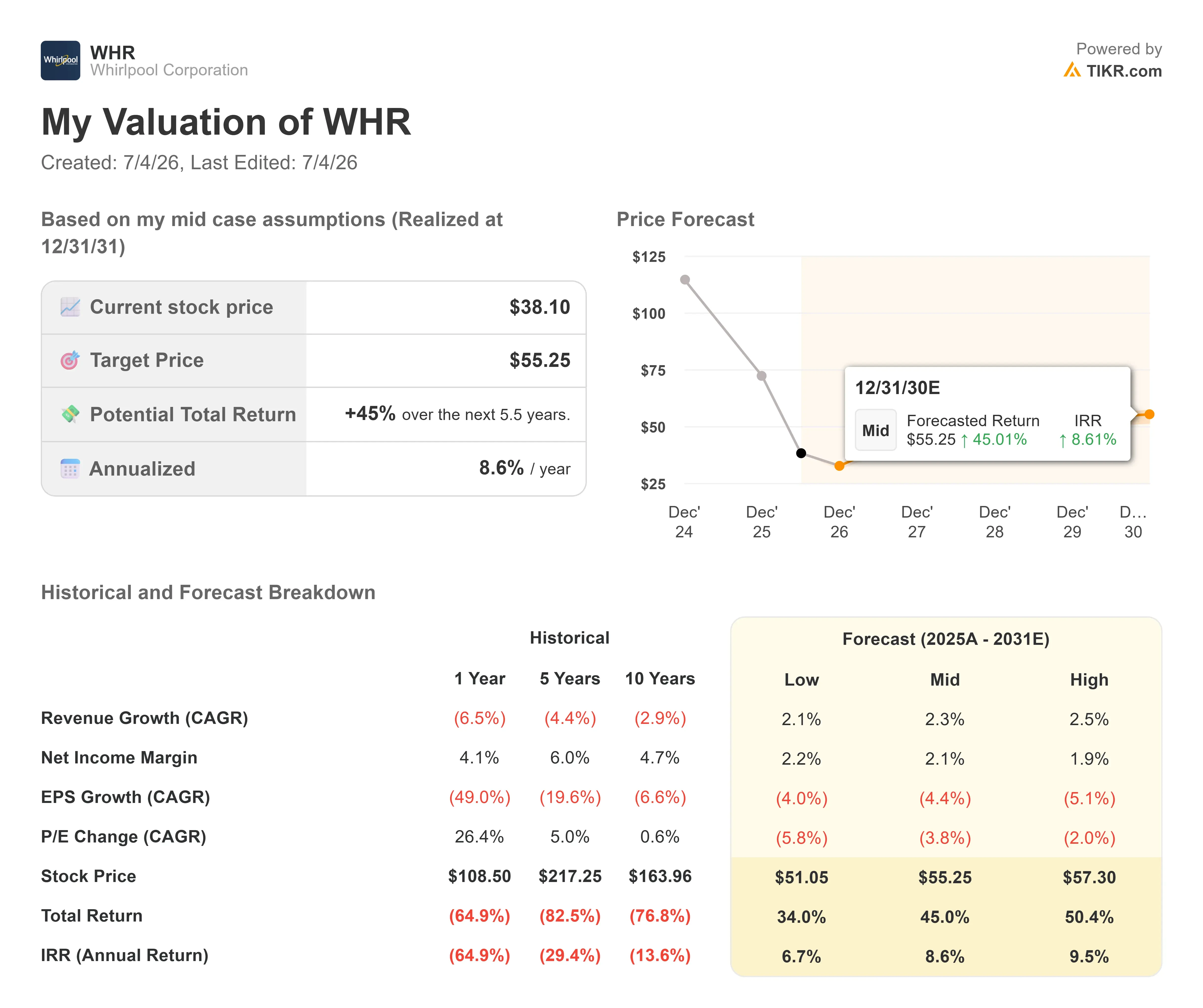

Here’s how WHR stock could perform under different scenarios by December 2030:

- Low Case: With revenue growing at 2.1% and net income margins of 2.2%, investors could see a total return of 34% (6.7% annually).

- Mid Case: At 2.3% revenue growth and 2.1% net income margins, the total return climbs to 45% (8.6% annually).

- High Case: If revenue grows at 2.5% and margins reach 1.9%, total returns could hit 50.4% (9.5% annually).

WHR Stock Valuation Model (TIKR)

WHR Stock Valuation Model (TIKR)

See what analysts think about WHR stock right now (Free with TIKR) >>>

The scenarios are tightly clustered because this is fundamentally a margin recovery story, not a growth story.

The key variables are whether pricing holds through the back half of 2026, how quickly consumer confidence recovers, and whether the Section 232 tariff framework stays in place long enough to drive lasting competitive advantage for domestic producers.

How Much Upside Does Whirlpool Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Kraken Enables Tokenized Stock Collateral for Leveraged Trades

Lawyers remain in disbelief over ‘fascist Hellscape’ July 4 display in DC

LIST: Bayanihan initiatives amid soaring oil prices