Marvell Is Up Around 260% in 2026 as It Joins the S&P 500. Here’s Where the Stock Could Go

Key Stats for Marvell Stock

- Current Price: $310.58

- Target Price (Mid): ~$865

- Street Target: ~$240

- Potential Total Return: ~180%

- Annualized IRR: ~25% / year

- Earnings Reaction: +18.35% (March 5, 2026)

- Max Drawdown: 26.42% (February 4, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Marvell Technology (MRVL) enters the biggest week of its decade with an awkward split. The stock is up around 265% in 2026. It joins the S&P 500 before the open on Monday, June 22, and yet Wall Street’s average price target still sits below where shares trade today. That gap is the argument. One side sees a company lapping its own analysts. The other sees a $272 billion chipmaker priced for a future that has to arrive on schedule.

The week of June 18 sharpened both views. KeyBanc lifted its target to a Street-high $385 and argued that Marvell’s optical networking, not its headline custom AI chips, is the more durable growth engine. The same stretch brought a new chief financial officer and an optics milestone, layered on the mechanical certainty of index-fund buying. The open question is whether an accelerating story can hold a stock this far above consensus once the forced buying clears.

What Happened in June

Three catalysts stacked inside two weeks. At COMPUTEX on June 2, NVIDIA CEO Jensen Huang called Marvell a candidate to become the “next trillion-dollar company,” and shares hit a record close of $316.43 on June 4. S&P Dow Jones Indices then confirmed Marvell would replace Pool Corp in the index on June 22. Finally, KeyBanc raised its target to $385 from $260 on June 18, and shares closed up 7.27% at $310.58 after touching $329.88 intraday.

The reaction is the tell. Marvell did not drift on the note; it jumped nearly 14% intraday before settling, which shows how tightly wound positioning is. You can review the company’s filings in its investor relations materials. There was a leadership change underneath, too: on June 11, Marvell named Dan Durn as chief financial officer, effective June 15. Durn arrives from Adobe with prior finance roles at Applied Materials, NXP, and GlobalFoundries, and the company reaffirmed its Q2 outlook alongside the news, signaling the handoff comes from strength.

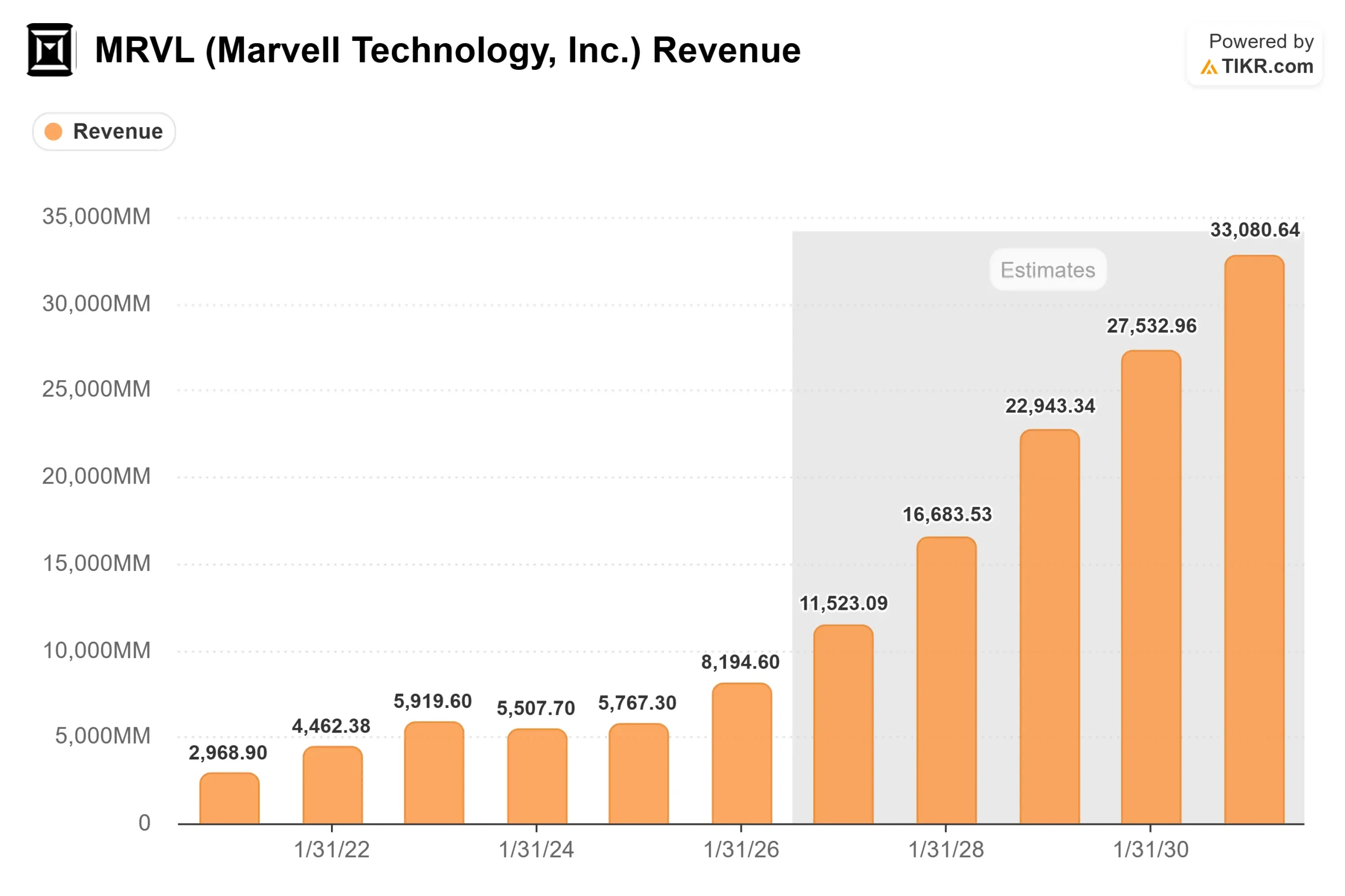

Marvell Revenue (TIKR)

Marvell Revenue (TIKR)

See historical and forward estimates for Marvell stock (It’s free!) >>>

The Optical-Versus-Custom Debate

KeyBanc touched the live nerve. For two years, the loudest part of the bull case has been custom silicon, the bespoke AI accelerators Marvell designs for individual hyperscalers. That business is tied to a small number of programs, which is the concentration risk bears keep circling. KeyBanc’s argument is that connectivity is the steadier engine.

CEO Matt Murphy made the same case at the Bank of America Global Technology Conference on June 3. He described Marvell as “majority is connectivity, not compute,” and said that is “one of the reasons why NVIDIA invested. We’re very complementary to the rest of the ecosystem.” That is why a rival like NVIDIA can also be a partner, and it is the structural reason the optical story may prove stickier than any single custom program.

There is a real new market behind the claim. Murphy pointed to scale-up switching, the connections inside one AI rack, as a market with no incumbent: “Scale-up switching is completely greenfield. It’s fully available. We could be leading the market from day 1.” On co-packaged optics, the revenue target for the next fiscal year has already doubled from $150 million at the time of the Celestial AI acquisition to $300 million. Backing that up, Tower Semiconductor and Marvell shipped over five million coherent photonic integrated circuits for data-center interconnects, a manufacturing milestone rather than a demo.

Why the Premium Is the Risk

The valuation question stays open. Marvell trades at around 54x NTM EV/EBITDA and around 69x NTM P/E. Per TIKR’s Competitors table, NVIDIA trades at around 17x and Broadcom at around 21x on the same EV/EBITDA basis, with the peer mean near 31x. Marvell carries a steep premium to the companies it partners with and competes against. That is only rational if it out-executes from a smaller base, which is the bet bulls are making.

The forward numbers justify the multiple, if anything does. TIKR data shows revenue growing from $8.2 billion in fiscal 2026 toward around $11.5 billion in fiscal 2027 and around $16.7 billion in fiscal 2028, a two-year forward CAGR of around 43%, the fastest in large-cap semiconductors. The bear worry is not a broken business. It is that a stock up around 265% this year already prices in most of what has to go right, leaving little room for a program delay or a hyperscaler spending wobble.

The Street is the clearest tell. The consensus mean sits around $240, below the current price, even after B. Riley raised its target to $345 and KeyBanc set the $385 high. The breakdown is 31 Buys, 7 Outperforms, 5 Holds, 1 Underperform, and 1 Sell: near-universal conviction in the business, deep disagreement on the price.

Marvell Street Targets (TIKR)

Marvell Street Targets (TIKR)

See how Marvell performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $310.58

- Target Price (Mid): ~$865

- Potential Total Return: ~180%

- Annualized IRR: ~25% / year

Marvell Advanced Valuation Model (TIKR)

Marvell Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Marvell stock (It’s free!) >>>

This is the mid case, and it sits above every published Street target, so treat it as the aggressive end of the range rather than a consensus view.

- Revenue drivers: interconnect scaling from 800G to 1.6T optical, and custom silicon at least doubling into fiscal 2028 as a second Tier 1 hyperscaler program ramps.

- Margin driver: operating leverage as revenue scales faster than costs, lifting net income margins toward the low 30s.

- Primary risk: concentration, since a handful of hyperscaler programs anchor the custom business.

The upside: Marvell delivers another upward revision, and scale-up switching turns greenfield market into revenue that the models do not yet carry.

The downside: data center growth decelerates, and the premium compresses toward the peer group, which would sting even if revenue keeps rising.

Conclusion

The index buying is mechanical and dated, so it fades by early July once the rebalance settles. After that, the stock trades on fundamentals, and the number that matters is the data center growth rate in Q2 fiscal 2027 earnings, due around August 27, 2026. Management has signaled that the rate is accelerating toward 55%. A print confirming that pace, with the $16.5 billion fiscal 2028 target reaffirmed, validates the premium and likely pulls lagging Street targets higher. A miss, or any stumble in the custom ramp, hands bears their case and exposes a stock at 54x EBITDA to a sharp repricing. Watch the August number, not the June index pop.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Marvell?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Marvell, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Marvell alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Marvell on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Bitcoin Pullback Bets Build as Saylor Signals Possible MSTR Accumulation

Jeanine Pirro's wild threat over Reflecting Pool sparks mockery: 'Going to get hilarious'

HYPE ETF Defies Market Gravity as BTC and ETH See Net Outflows