The next crypto recovery trade might be equities instead of tokens

The total crypto market cap is down more than 36% year over year, the altcoin complex sits roughly 45% below its October 2025 peak, and Bitcoin is on course for its worst annual start in more than a decade, with capital rotating into AI stocks and major IPOs.

Three years of waiting for a broad altseason that never arrived have left altcoin traders with fast-decaying narratives, unlock-driven selling, memecoin rotations that rewarded a handful of early buyers, and rallies that faded before most participants could size in.

Some investors are now asking whether owning the companies that profit from crypto activity is a cleaner trade than picking the next token.

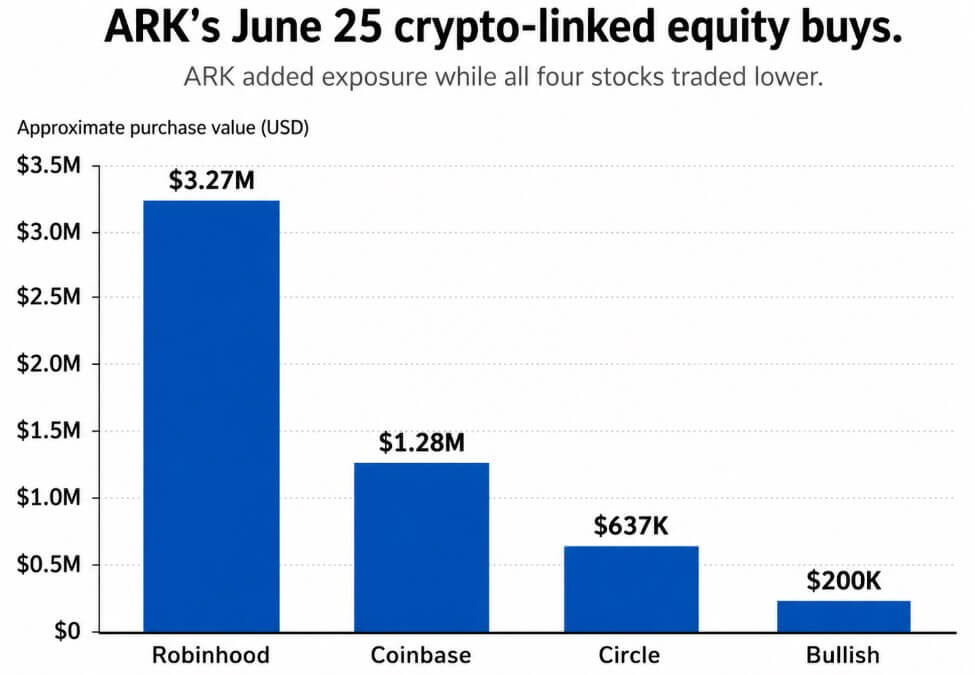

On June 25, ARK's ETFs bought roughly $5.4 million in four crypto-linked equities, even as all four stocks traded lower.

The purchases totaled approximately $1.28 million on Coinbase, $637,455 on Circle, $199,895 on Bullish, and $3.27 million on Robinhood. Cathie Wood was buying into weakness, and the stocks she chose are companies that monetize crypto activity.

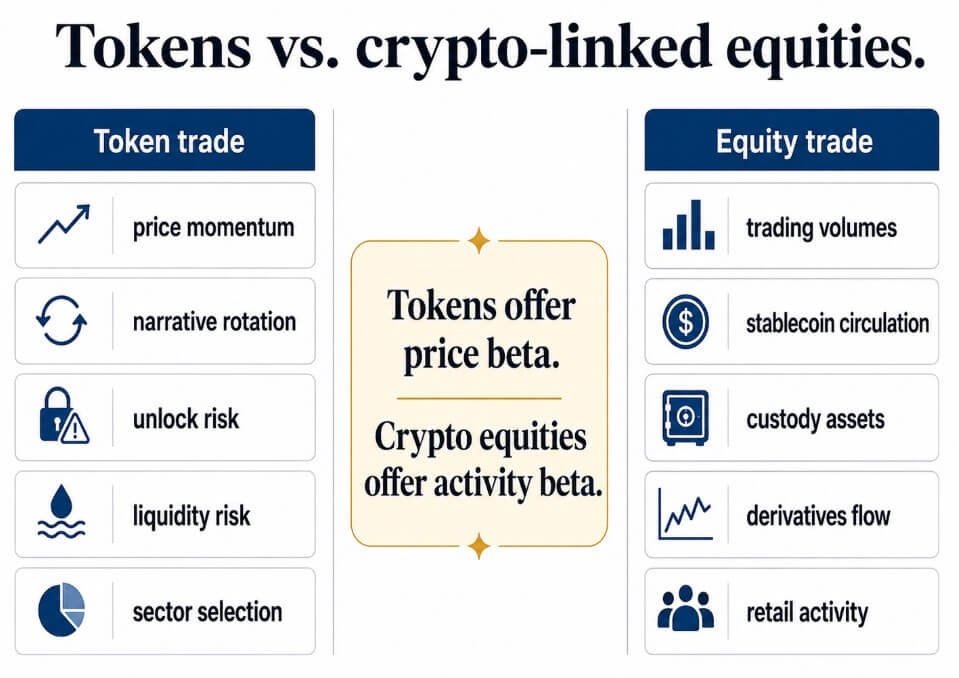

Crypto-linked equities give investors exposure to crypto activity, including trading volumes, stablecoin circulation, custody assets, derivatives flows, and retail speculation.

In the kind of low-energy chop that has defined the past three years, the two bets diverge sharply.

ARK invested roughly $5.4 million across four crypto-linked equities on June 25, led by $3.27 million in Robinhood, while all four stocks traded lower.

ARK invested roughly $5.4 million across four crypto-linked equities on June 25, led by $3.27 million in Robinhood, while all four stocks traded lower.

What each name represents

Coinbase's first-quarter update reported crypto trading volume market share at 8.6%, derivatives trading volume up 169% year over year on a trailing-twelve-month basis, and 12% of global crypto assets in custody, with more than 25% of USDC in circulation held in Coinbase products.

Those structural positioning numbers reflect what Coinbase collects when volumes return and how exposed it is when they recede.

Coinbase's transaction revenue for the period fell approximately 40% to $756 million, total revenue dropped to $1.43 billion from $2.03 billion a year earlier, and the company posted a second consecutive quarterly loss as trading momentum faded.

Circle's USDC circulation reached $77 billion in the first quarter, up 28% year over year, while on-chain USDC transaction volume rose 263% to $21.5 trillion.

Total revenue and reserve income came in at $694 million, up 20%, driven by higher average USDC circulation, partly offset by a lower reserve return rate. Live data as of June 25 showed $73.6 billion USDC in circulation.

Circle's economics run on circulation size, reserve yields, and distribution arrangements, with altcoin narrative cycles carrying no weight in that model.

Every 100 basis points of gross reserve-yield movement on $77 billion in circulation equals roughly $770 million annualized before costs.

CRCL trades as a rates-and-dollar-liquidity bet layered atop a stablecoin adoption bet, with a risk profile shaped primarily by interest rates and regulatory outcomes.

Robinhood's crypto revenue came in at $134 million in the first quarter, down 47% year over year, and Robinhood App's crypto notional trading volume fell 48%, with an additional $42 billion from Bitstamp bringing the total notional to $66 billion.

Bullish rounds out the basket on the institutional side, reporting digital asset sales of $51.8 billion in the first quarter, adjusted EBITDA of $35.1 million, and 14% open-interest market share in BTC options in April.

| Company | Crypto exposure | What has to return | Main risk |

|---|---|---|---|

| Coinbase | Exchange fees, custody, derivatives, USDC economics | Trading volume, institutional activity, retail speculation | Revenue falls quickly when volumes fade |

| Circle | USDC circulation, reserve income, payments infrastructure | Stablecoin adoption, supportive rates, regulatory clarity | Lower rates or distribution costs compress economics |

| Robinhood | Retail crypto brokerage, app-based speculation, Bitstamp volume | Retail risk appetite and crypto notional volume | Retail flow can disappear fast in low-energy markets |

| Bullish | Institutional exchange infrastructure, digital asset sales, BTC options | Institutional trading demand and derivatives activity | Institutional volumes contract when crypto sentiment weakens |

The trade that follows

In the bull case, retail speculation returns, derivatives activity recovers, and stablecoin supply continues to expand.

Under those conditions, exchanges and brokers may reprice before broad altcoin rotation becomes obvious, because transaction revenue and earnings estimates can reset faster than token narratives form.

Coinbase adding 10% to its transaction revenue base of $756 million in the first quarter means roughly $76 million more per quarter, and that figure reaches $189 million at 25%.

The companies collecting fees from renewed activity can move forward with estimates before anyone agrees on which L1, L2, or sector token to own.

In the bear case, AI, IPOs, and public-market equities continue to absorb capital, crypto volumes stay thin, and the narrative churn that has defined the past three years continues.

When activity fades, public crypto firms feel it directly in revenue, as Coinbase and Robinhood's recent results already show.

Circle depends on USDC circulation holding and reserve yields staying supportive, and Bullish depends on institutional trading demand that can itself contract when broader crypto sentiment turns.

A prolonged crypto winter leaves every one of these businesses earning well below full capacity.

Tokens offer price beta through momentum and unlock risk; crypto equities offer activity beta through volumes, stablecoins, custody, and retail flow.

Tokens offer price beta through momentum and unlock risk; crypto equities offer activity beta through volumes, stablecoins, custody, and retail flow.

The old version of the rebound thesis trade required picking a token before retail found it, accepting the liquidity risk, the unlock schedule, the narrative decay, and the possibility that rotation passed through a separate sector entirely. The equity version trades token-level upside for a more legible bet on activity itself.

Whether this cycle's rotation looks like 2021's broad altseason or something narrower, faster, and harder to ride from the token side is the question Wood is already positioned on the equity side of.

The post The next crypto recovery trade might be equities instead of tokens appeared first on CryptoSlate.

추천 콘텐츠

Iran’s foreign minister targeted in assassination attempt, wife killed

Trump insiders reveal he 'isn't sold' yet on his biggest 2028 decision

The Trade Desk Is Down 51% in 2026. Is the Multiple Finally Cheap Enough?

인기 뉴스

더보기