Why Salesforce Stock at $153 Deserves a Second Look After Record EPS and Buybacks

Key Takeaways for Salesforce Stock as of June 2026

- Analysts rate Salesforce stock 32 Buy, 6 Outperform, 10 Hold, 2 Underperform, and 2 Sell, with a street mean target of $252, implying around 64% upside from the current price of $153.

- TIKR’s mid-case model values Salesforce at around $296 by January 2031, implying around 93% total return from current levels, or roughly 15% annualized.

- Salesforce stock is undervalued at current levels, with non-GAAP EPS of $3.88 growing 50% year-over-year in Q1 FY2027 while the stock trades near its 52-week low of $146.

- Agentforce annual recurring revenue topped $1.2 billion in Q1 FY2027, up 205% year-over-year, the fastest-growing product in Salesforce’s history.

Most investors never know if a stock is truly undervalued or overpriced. TIKR’s professional-grade valuation tools give you a clear, data-backed answer across 60,000+ stocks for free →

Salesforce Stock Plunges to a 52-Week Low While the Business Posts Record Numbers

CRM Stock Q1 2026 Earnings in USD (TIKR)

CRM Stock Q1 2026 Earnings in USD (TIKR)

Salesforce, Inc. (CRM) trades at $153, a near-record disconnect between stock price and operating performance, after the company delivered Q1 FY2027 revenue of $11.133 billion, a 13% year-over-year gain that beat the $11.057 billion consensus, while non-GAAP EPS of $3.88 crushed the $3.13 estimate by 24%.

The world’s largest CRM software company serves more than 150,000 enterprises globally with cloud-based sales, service, marketing, and data management platforms, and its AI agent layer, Agentforce, crossed $1.2 billion in annual recurring revenue during the quarter, up 205% year-over-year.

The market shrugged.

Salesforce stock fell in the after-hours session and spent 2026 absorbing the fear that AI coding tools from Anthropic and OpenAI will let enterprises build their own replacements for Salesforce’s software, hollowing out the per-seat subscription model that generates $46 billion in annualized revenue.

CEO Marc Benioff addressed this directly on the Q1 earnings call, noting that Anthropic calls Slack its “core operating system” and uses Sales Cloud more intensively than most of Salesforce’s traditional enterprise customers.

The Fin acquisition, a $3.6 billion deal for an autonomous AI customer-service agent platform with 30,000 customers, signals that Salesforce intends to compete for agentic workloads rather than defend against them.

Headless 360, launched at the March developer conference, opens the entire platform to external AI agents through the Model Context Protocol, and the company processed 4.5 million MCP calls through Q1.

The $25 billion accelerated share repurchase retired 103 million shares in Q1, representing 11% of shares outstanding, and the company returned $27.5 billion to shareholders in a single quarter while raising full-year FY2027 revenue guidance to $45.9 billion–$46.2 billion.

See the exact moment Wall Street upgrades a stock before the rest of the market piles in — track analyst rating changes in real time with TIKR for free →

Salesforce Stock Consensus Stays Bullish at $252 as the EPS Trajectory Widens the Disconnect

CRM Stock Revenue and EPS Actuals & Estimates (TIKR)

CRM Stock Revenue and EPS Actuals & Estimates (TIKR)

Wall Street expects Salesforce stock to deliver around 10% constant-currency revenue growth in Q2 FY2027, with consensus estimating quarterly revenue of around $11.32 billion, and the earnings picture looks considerably stronger than the revenue line alone suggests.

Salesforce stock’s non-GAAP EPS consensus for Q2 FY2027 stands at around $3.27, and full-year FY2027 consensus projects non-GAAP EPS of around $14, a trajectory compounding from a business generating record quarterly free cash flow.

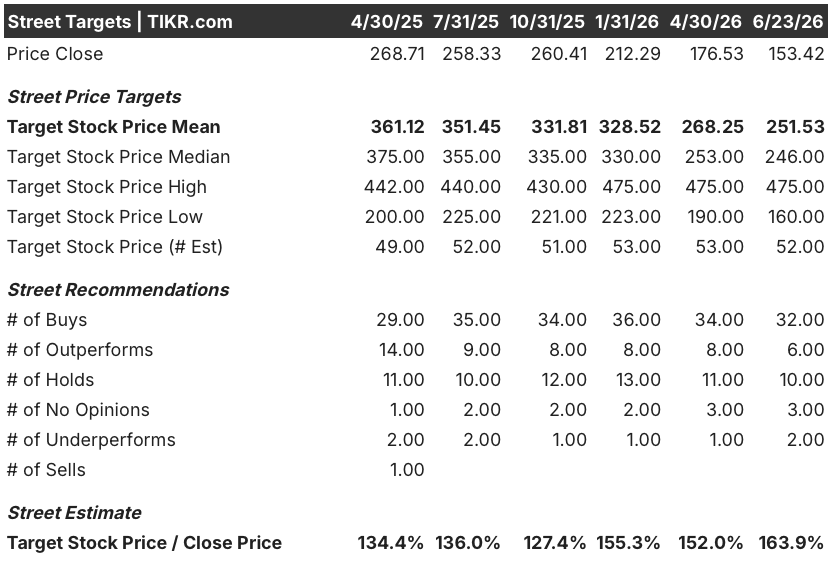

Street Analysts Target for CRM Stock (TIKR)

Street Analysts Target for CRM Stock (TIKR)

Thirty-two analysts rate Salesforce stock a Buy, six rate it Outperform, and ten rate it Hold, with a street mean price target of $252, implying around 64% upside from $153, and the street high target stands at $475.

The loudest bear case comes from BofA, which argues Salesforce faces a structural shift that permanently impairs its business model, a view shared by just two analysts in a coverage universe of 52, with bears pointing to Q2 guidance landing slightly below the $11.36 billion consensus as evidence that organic subscription growth stays under pressure.

A business delivering 50% non-GAAP EPS growth with a $14 full-year earnings trajectory does not trade at 11 times forward earnings unless the market expects that trajectory to collapse, and the Agentforce adoption data argues it will not, which is why Salesforce stock looks undervalued at $153.

The unresolved question is timing, specifically whether the H2 FY2027 organic subscription revenue reacceleration materializes on schedule and whether Agentforce and Fin convert adoption into booked subscription revenue before Tableau and Commerce Cloud drag the headline longer.

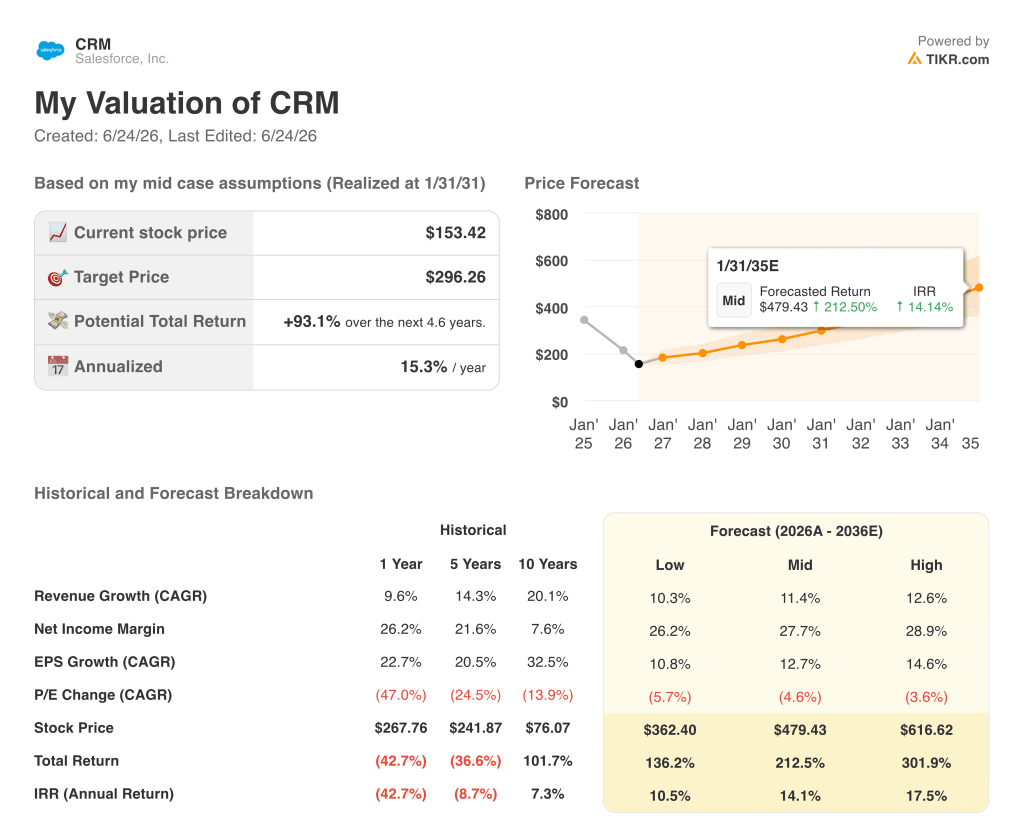

Is Salesforce Stock Undervalued in 2026? TIKR’s $296 Target Says the Gap Is Significant

TIKR’s mid-case values Salesforce at approximately $296 by January 2031, implying around 93% total return from the current price of $153, or roughly 15% annualized over approximately 4.6 years.

CRM Stock Valuation Model Results (TIKR)

CRM Stock Valuation Model Results (TIKR)

The TIKR target rests on compounding engines that Q1 FY2027 data already validates, including Agentforce ARR growing 205% year-over-year, a $25 billion buyback reducing share count by 11% in a single quarter, and non-GAAP operating margin holding at 34.8% while the company simultaneously absorbed Informatica, Fin, m3ter, and Contentful.

Salesforce stock’s quarterly free cash flow of $6.556 billion running at a rate that far exceeds annual capital expenditures means the company funds its entire acquisition and buyback program without impairing the core cash generation engine, and that durability is what the TIKR target depends on most directly.

If management’s guided H2 organic subscription revenue acceleration arrives late or falls short, the path to $296 extends in time without necessarily breaking, and the $252 street mean target already prices in a more conservative path toward the same direction.

Wall Street’s best ideas don’t stay hidden for long. Catch analyst upgrades, earnings beats, and revenue surprises on thousands of stocks the moment they happen with TIKR for free →

Should You Invest in Salesforce, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Salesforce, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Salesforce, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CRM stock on TIKR for Free →

추천 콘텐츠

Binance Withdraws MiCA License Application in Greece, Eyes Reapplication in Other EU States

Can You Sell Covered Calls on Leveraged ETFs for Income? Yes, But The Yield Is Risky

'Lost my temper': Republican spills on his blowup with Trump

인기 뉴스

더보기