McDonald’s at 52-Week Low: Buy, Sell or Hold?

The post McDonald’s at 52-Week Low: Buy, Sell or Hold? appeared first on 24/7 Wall St..

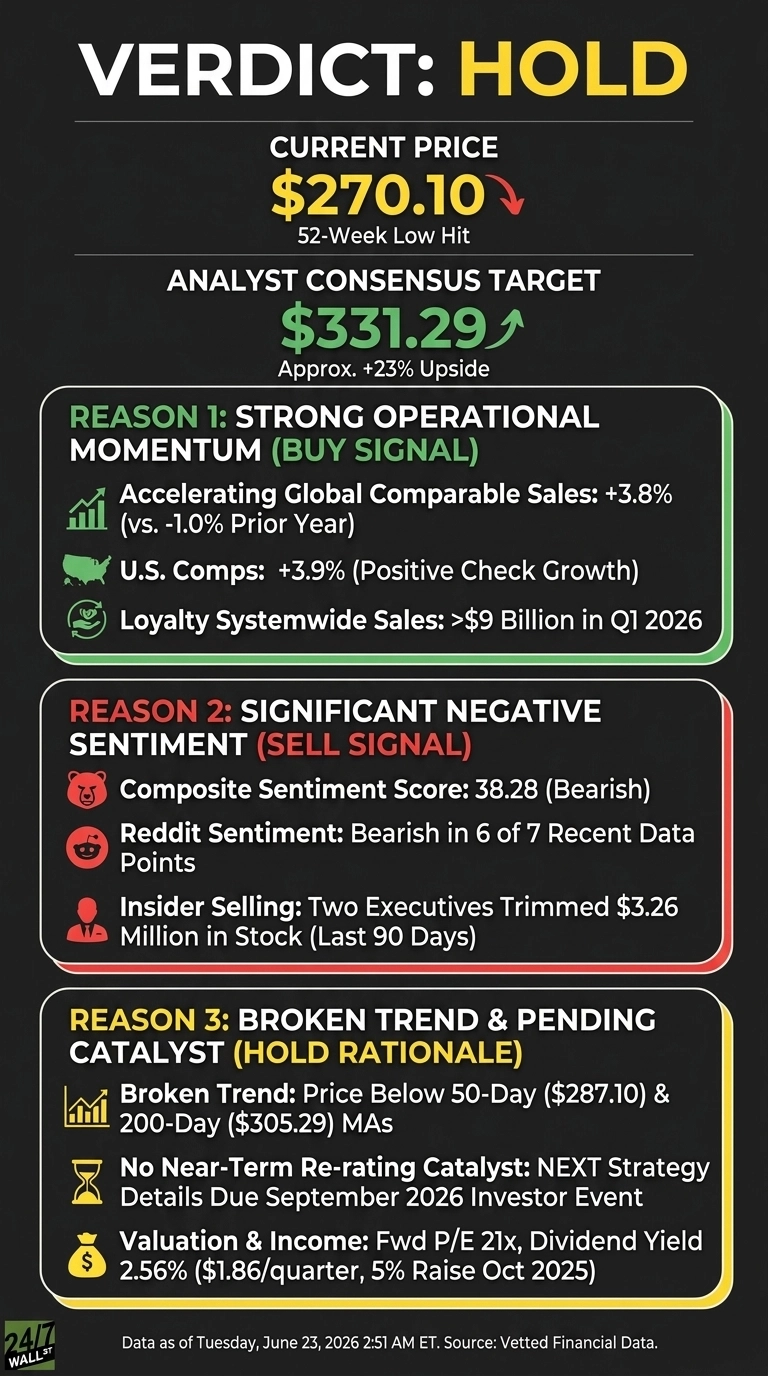

- McDonald's (MCD) at $270.10 looks compelling with accelerating comps while trading at 52-week lows despite strong fundamentals.

- McDonald's fourth straight quarter of accelerating global comparable sales provides the strongest support for the bullish thesis.

- Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and McDonald's didn't make the cut. Grab the names FREE today.

At $270.10, McDonald’s (NYSE:MCD) looks compelling to research. The stock just hit a fresh 52-week low while the underlying business is posting its fourth straight quarter of accelerating global comparable sales, a setup that rarely lasts long.

McDonald’s is the world’s largest restaurant franchisor, with more than 45,000 restaurants across over 100 countries and a roughly 95% franchised model that produces stable, high-margin rent and royalty income.

The stock has slid from a 52-week high of $337.56 to a 52-week low of $270.15, dragged lower by sector-wide margin worries, insider selling, and weakness across restaurant names. The fundamentals tell a different story than the chart.

Why the chart looks worse than the business

Q1 2026 delivered EPS of $2.83 against a $2.7446 estimate, with revenue of $6.52 billion growing 9.44% year over year. Global comps came in at +3.8% versus -1% a year ago, U.S. comps at +3.9%, and loyalty systemwide sales topped $9 billion in the quarter on a base of $38 billion trailing.

Valuation has compressed alongside the price. The stock trades at a forward P/E of 21x, with a 2.56% dividend yield backed by Aristocrat status and a 5% raise in October 2025 to $1.86 per quarter. SG Americas boosted its stake 68.9% to roughly $299.5 million, and analyst consensus sits at a $331.29 target with 19 Buy, 14 Hold, and 1 Sell ratings.

Why bears think this is a value trap

The sell case centers on margins. Peers are showing real pressure: Chipotle’s restaurant-level operating margin fell to 23.7% from 26.2%, and the USDA is flagging higher farm input costs. McDonald’s faces its own headwinds, including restructuring charges running through 2027, 4% to 6% higher interest expense, and a 22.0% effective tax rate versus 19.8% prior year.

Sentiment is hostile. The composite sentiment score reads 38.28 (Bearish), Reddit chatter has run bearish in 6 of 7 recent data points, and two executives trimmed $3.26 million in stock over 90 days. Momentum is negative across every window inside one year.

Why patient investors might want to wait

The hold camp has a point. The 50-day moving average sits at $287.10 and the 200-day at $305.29, so the trend is broken. With the NEXT strategy financial details not due until the September investor event, there is no obvious near-term catalyst to force a re-rating. A weaker consumer or another legal flare-up could push shares lower before they bottom.

What the numbers say at the 52-week low

MCD currently trades at $270.10 against an analyst target of $331.29, implying roughly 23% upside, with 19 Buy ratings, 14 Hold, and 1 Sell across 34 analysts.

Shares are down 10.53% year to date and 3.76% over the past year, while since the May 7 earnings filing MCD has fallen 5.85% versus SPY’s 1.75% gain. Trailing P/E sits at 23x with a beta of 0.414.

24/7 Wall St.

24/7 Wall St.

At $270.10, the bull case for McDonald’s

Comps have accelerated for four straight quarters, value-led traffic is positive in the U.S., and international operated markets grew revenue 14% year over year. With 2,600 new restaurants planned in 2026 and a mid-to-high 40% operating margin target, the earnings power compounds even without multiple expansion.

Risk/reward at the low is asymmetric. A 21x forward multiple on a defensive cash machine generating $7.19 billion in 2025 free cash flow and a 2.67% growing dividend offers income while the thesis plays out. The September NEXT investor event is the most likely near-term catalyst to re-rate the multiple.

What would invalidate the thesis: a deceleration in global comps back below 2%, U.S. traffic turning negative, or a material guide-down on operating margin. Watch comps, company-operated margin, and loyalty sales growth quarter to quarter.

When the world’s most durable franchise model trades at a 52-week low while comps accelerate, history suggests the setup has rewarded patient holders.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and McDonald’s didn’t make the cut. Grab the names FREE today.

The post McDonald’s at 52-Week Low: Buy, Sell or Hold? appeared first on 24/7 Wall St..

You May Also Like

Semiconductor Stocks Tumble: Nvidia (NVDA), AMD, and Micron Face Sharp Declines

Critical USDT0 Response to Drift Hack Exposes Stark Contrast in Stablecoin Security Protocols

China Nabs Another Huione Group Core Member in Cambodia Extradition